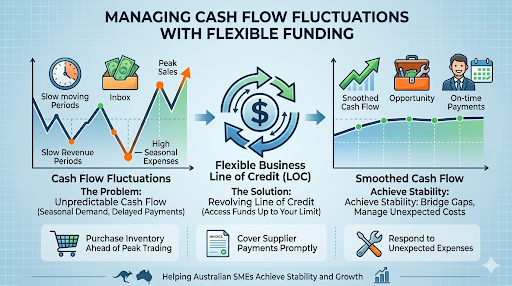

Cash flow rarely moves in a perfectly straight line. Even well-established businesses can experience periods where expenses increase temporarily or incoming revenue slows down.

For many companies, maintaining access to flexible capital can help smooth these fluctuations without requiring a new loan application each time funds are needed.

One option often considered by Australian SMEs is a business line of credit in Australia.

This type of facility operates differently from traditional term loans. Instead of receiving a lump sum upfront, businesses are approved for a credit limit that they can access whenever required.

How a Line of Credit Works

A line of credit functions similarly to a revolving facility.

Once approved, the business can draw funds up to the agreed limit and repay them over time. When repayments are made, the available balance becomes accessible again.

This structure can be particularly useful for businesses that experience:

- seasonal revenue patterns

- unpredictable operating costs

- fluctuating inventory requirements

- delayed client payments

Rather than applying for multiple loans, a single facility can provide ongoing access to working capital.

Typical Uses for Flexible Credit

Businesses often use this type of funding for operational needs rather than long-term investments.

Common uses include:

- purchasing stock ahead of peak trading periods

- covering supplier payments

- managing short-term cash flow gaps

- responding to unexpected expenses

Because funds can be drawn only when required, businesses maintain greater control over how much capital they use.

Benefits of Revolving Access to Capital

One of the main advantages of a revolving facility is flexibility.

Instead of committing to a fixed loan amount, businesses can access smaller amounts as needed. This allows companies to adjust borrowing according to changing circumstances.

For example, a business may draw funds to purchase inventory before a busy season and then repay the balance once sales revenue increases.

This ability to adjust borrowing levels can reduce the need for repeated loan applications.

Points to Consider Before Applying

While flexible funding can be helpful, businesses should review how the facility will fit into their overall financial strategy.

Considerations may include:

- how frequently the credit line will be used

- repayment expectations during slower periods

- existing loan commitments

Understanding how the facility integrates with daily cash flow management is essential.

Summary

Access to flexible capital can help businesses navigate uncertain periods while continuing to operate smoothly. However, the value of any funding solution depends on how well it aligns with the business’s revenue cycle and operational needs.

At Lend Brokers, we work with Australian businesses to review their cash flow patterns and identify funding structures that support stability and growth. Careful planning before accessing credit can help ensure the facility becomes a useful financial tool rather than an additional financial burden.

{kind=link}